Featured Post

Who Can Own a Medical Spa?

Clinical

By Belmar Pharma SolutionsWhen it comes to menopause, a once-taboo topic, the tide has finally changed. Women now have access ...

AmSpa Events

New technologies, regenerative treatments, and innovative business solutions. If you want to stay ahead of the curve, Medical Spa Show ...

Business

By Medical Marketing WhizAs the year comes to a close, now is the perfect time to reflect on what’s working—and ...

AmSpa Events

Successful med spas build teams that grow together. That’s why Medical Spa Show 2026 (MSS26) is designed for entire practices ...

Marketing

By AestheticsPro For medical spa owners looking to reach their clients in the most...

Top Tags

January 24, 2023

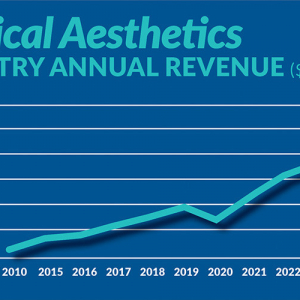

Figure displays medical aesthetics industry annual revenue ($ in billions). By Madilyn Moeller Day-to-day life...

February 24, 2021

By Bradford E. Adatto, Partner, ByrdAdattoIntravenous (IV) therapy has been used to provide nutrition and...

September 21, 2023

By Patrick O'Brien, JD, General Counsel, American Med Spa Association [AmSpa first published a...

July 19, 2023

By Patrick O'Brien, General Counsel, American Med Spa Association (AmSpa) UPDATE #2 (2/08/2024): Since...