Featured Post

Who Can Own a Medical Spa?

AmSpa Events

The first few years of operating a medical spa can be exciting and, at the same time, overwhelming. Nearly half ...

AmSpa Events

The Medical Spa Show 2026 is gearing up to deliver its most dynamic, innovation packed exhibit hall yet, with more ...

AmSpa Events

Med spa technology is advancing quickly. Electronic medical records, EMR, customer relationship management, CRM, lead management systems, LMS, automated marketing ...

Clinical

By Belmar Pharma SolutionsYour bustling, successful practice is full of women who really care about their appearance, and they trust ...

Marketing

By AestheticsPro For medical spa owners looking to reach their clients in the most...

Top Tags

January 24, 2023

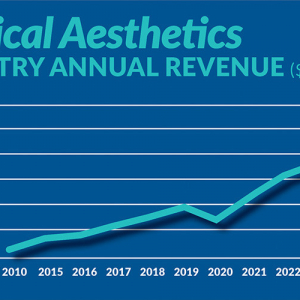

Figure displays medical aesthetics industry annual revenue ($ in billions). By Madilyn Moeller Day-to-day life...

February 24, 2021

By Bradford E. Adatto, Partner, ByrdAdattoIntravenous (IV) therapy has been used to provide nutrition and...

September 21, 2023

By Patrick O'Brien, JD, General Counsel, American Med Spa Association [AmSpa first published a...

July 19, 2023

By Patrick O'Brien, General Counsel, American Med Spa Association (AmSpa) UPDATE #2 (2/08/2024): Since...