Featured Post

Who Can Own a Medical Spa?

Legal

In Indiana, a senate bill regulating med spas and GLP-1 compounding recently passed and was signed into law. Here's what ...

AmSpa Events

By Adam Reinebach, Chief Executive Officer, American Med Spa Association (AmSpa)For many med spa owners, there’s a moment where the ...

Marketing

By Aesthera MarketingThe way people choose a med spa today looks nothing like it did a few years ago. Many ...

AmSpa Events

By Adam Reinebach, Chief Executive Officer, American Med Spa Association As we close the first quarter of 2026, more people are ...

Marketing

By AestheticsPro For medical spa owners looking to reach their clients in the most...

Top Tags

January 24, 2023

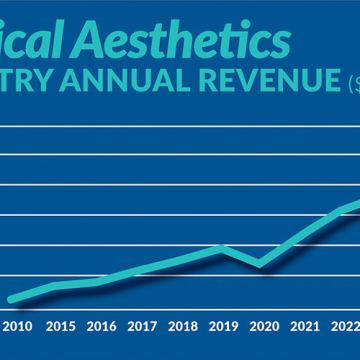

Figure displays medical aesthetics industry annual revenue ($ in billions). By Madilyn Moeller Day-to-day life...

February 24, 2021

By Bradford E. Adatto, Partner, ByrdAdattoIntravenous (IV) therapy has been used to provide nutrition and...

September 21, 2023

By Patrick O'Brien, JD, General Counsel, American Med Spa Association [AmSpa first published a...

July 19, 2023

By Patrick O'Brien, General Counsel, American Med Spa Association (AmSpa) UPDATE #2 (2/08/2024): Since...